EssaysVolume5

Trade, Investment, and Payments

Richard A. Stanford

Furman University

Greenville, SC 29613

Copyright 2024 by Richard A. Stanford

stored, or transmitted by any means without written permission

of the author except for brief excerpts used in critical analyses

and reviews. Unauthorized reproduction of any part of this work

is illegal and is punishable under the copyright laws of the

United States of America.

CONTENTS

Introduction

1. The Dimensions of Global Commerce

2. The Theory of Trade

3. Barriers to Trade

4. Industrial Policy

5. The Multinationalization of Enterprise

6. Opportunities in Developing Economies

7. Government and International Commerce

8. External Balance

9. Exchange Rates

10. Payments Imbalances

11. Deficits and Surpluses

Return to START Menu

This essay set presents the theories of interregional trade and payments that underlie international commerce. Two recurring themes are that automatic adjustment mechanisms, if left alone, would alleviate trade and payments issues, and that politically inspired policies to affect trade and payments often disrupt the automatic adjustment mechanisms and prevent them from working.

The term "globalization" has come into wide-spread usage during the early years of the twenty-first century. The more commonly used terms prior to the present century were "international trade" and "international investment." It will be convenient to continue employing these terms to describe the global dimensions of commerce.

The theory of specialization according to comparative advantage is based upon interregional relationships. It abstracts completely from the international identities of the regions. However, the theory requires a highly abstract aggregate perspective that may appear to be unrelated to the microeconomic decision realities. In the following presentation, we shall lay out the theory of interregional trade and make connections to the decision realities where possible. Even though an aggregate perspective is required, the analysis employs various microeconomic concepts that must be generalized to the level of aggregate or industry behavior.

Isoquant Q14 (and its fellows in the map) is "well behaved" so that the technology which it illustrates is neither particularly capital nor labor intensive. By way of contrast, isoquant Q14 in panel (a) of Figure 2-1 illustrates a technology that is labor intensive relative to that illustrated by isoquant Q24 in panel (b). Along Q14 a relatively small decrement in the use of capital must be offset by a large increment in the use of labor in order to remain at the same level of output. Compared to Q14, Q24 in panel (b) illustrates a relatively more capital intensive technology because along Q24 a small decrement of labor requires a relatively larger increment of capital in order to remain at the same level of output. These factor intensity relationships are important to the subsequent argument that regional comparative advantages may be based (among other possibilities) in the choice of technology according to its relative factor intensity.

Along isoquant Q34 above point G the technology is relatively capital intensive, and capital is less substitutable for labor in the sense that if the labor input is decreased only slightly from L35 to L36, a large amount of additional capital (from K35 to K36) is required in order to remain at the same level of output. Along Q34 to the right of point H, the technology is relatively labor intensive, and labor is less substitutable for capital in the sense that if the capital input is decreased only slightly from K37 to K38, a larger amount of additional labor (from L37 to L38) is required in order to remain at the same level of output.

The isoquant map for industry A's production process is oriented toward the lower-left origin, 0A. The positive directions of change from origin 0A are as normally expected in bivariate graphic analysis. Because its isoquants are relatively steeply sloped, we can infer that item A is produced with a relatively capital intensive technology.

These quantity and cost considerations are then the bases for concluding that Inland has a comparative advantage in the production of item B while Outland has a comparative advantage in the production of item A. However, even if one of the regions, say Inland, had a cost or output advantage in the production of both goods relative to Outland, we could still designate Inland's and Outland's comparative advantages. Inland's comparative advantage lies with the industry possessing the greatest absolute advantage, while Outland's comparative advantage lies with its industry possessing the least absolute disadvantage.

The Inland society's iso-welfare map has been brought forward from panel (b) of Figure 2-3 to be situated in the box relative to Inland's origin in the lower left corner. The Outland society's iso-welfare map has been brought forward from panel (b) of Figure 2-4, rotated 180 degrees, and situated relative to Outland's origin in the upper-right of the box. The tangencies of Inland and Outland iso-welfare curves trace out the path from the Inland origin through points D, G, and E to the Outland origin. This path is usually referred to as a "contract curve" (not to be confused with the "maximum efficiency locus" in the production box diagram) because negotiation between the Inland and Outland societies can be expected to conclude with a contract for redistribution of A and B at some point along the path.

As can be seen in Figure 2-6, Inland generalizes both its production and consumption at point S' prior to the initiation of interregional trade with Outland. Once terms of trade negotiations are completed, Inland begins a process of increased production specialization in its comparative advantaged product, item A, by moving along its production possibilities curve from point S' to point T'. Inland then exports quantity (B2-B1) of its B output to Outland in exchange for an import of quantity (A3-A1) of A. Even though Inland has increased its specialization in the production of item B, through interregional trade it is able to generalize its consumption with the combination of B3 and A3, achieving iso-welfare level W4, which is a significant gain from trade relative to the welfare possibility (W3) in the absence of trade. It may be said that Inland has moved around its "trade triangle" from T' to V to Z, thus achieving a higher level of welfare by increasing specialization in its comparative advantaged product and trading off some of its additional production.

In Chapters 1 and 2 we made the case that specialization by comparative advantages together with free trade among regions can increase and ultimately maximize global welfare. This chapter examines the implications for welfare among trading partners if trade is encumbered by trade barriers. It is therefore necessary to shift our attention from interregional to international trade and assume the existence of governments that are both interested in and capable of imposing barriers to trade with other nations.

If the economy has been closed to international commerce, opening it to trade will make foreign-made products available to domestic consumers.

Or, a foreign-made supply of the product whose market conditions are represented in Figure 3-1 may become available in a second product life-cycle phase as production begins in so-called "imitator countries." Sw in Figure 3-2 depicts an initial small foreign (or "world") supply to a relatively large domestic economy. This small world supply is fairly inelastic with respect to price. Assuming that no trade barriers are imposed, the total supply available for consumption domestically is represented by the supply curve Sd + Sw, which is located in coordinate space as the horizontal summation of Sd and Sw.

Consequent upon the opening of trade to import of the foreign supply of the good, the domestic market price of the good falls from P1 to a new equilibrium at P2. At the lower price P2, the amount of domestic production falls from Q1 to Q2. The total quantity transacted in the domestic market increases from Q1 to Q3. Domestic producers are unhappy at the opening of foreign trade for import of the product; their sales revenue falls from the area of the rectangle represented by corner points 0Q1AP1 to the area of the rectangle identified by corner points 0Q2BP2. But consumers are happy that they can now purchase the larger Q3 quantity of the good at the lower price P2. Their consumer surplus increases by the amount of the triangular area m.

Once the tariff is imposed, the market price rises from P2 to P3. Domestic producers are all too happy to accept the higher price P3 although it is still not as high as the pre-trade price of P1. Domestic production increases from Q2 to Q4. At the higher market price, domestic consumption falls from Q3 to Q5, and domestic consumers of the product suffer a decrease of consumer surplus represented by the small triangular area below line segment FC. The quantity of the product imported decreases from (Q3 - Q2) to (Q5 - Q4). These effects are relatively small since the world supply Sw is fairly inelastic with respect to price, but the effects will become larger as Sw increases and becomes more elastic.

Domestic producers can be expected to appeal for protection. Domestic consumers should oppose any such protection measures on grounds that they will pay a higher price for the product, less of it will be available in the market, and their consumer surplus will shrink. Unfortunately, consumers typically are less well organized than producers who lobby for protection. In the Figure 3-4 illustration, the government could impose a tariff of any magnitude ranging from nearly zero to the full amount of the difference between P11 and P12. A tariff equal to this full difference would be sufficient to choke off all imports of the product. If the same tariff as illustrated in Figure 3-3 is imposed on the horizontal world supply curve in Figure 3-4, the tariffed supply curve will lie in position Sw + tariff, causing market price to rise to P13.

A quota is one type of "non-tariff barrier" (NTB) to trade. Other forms of NTB include performance, national origin, packaging, safety, and health requirements. If any NTB is imposed upon imports from a trading partner, the dimensions of the trade triangles in Figure 2-6 of Chapter 2 will be decreased. The result is that lower levels of welfare than those at point Z will be attained by both trading partners.

4. Industrial Policy A standard premise underlying the teaching of economic theory in "the West" is that markets are superior structures of economic organization for revealing and serving the preferences of populations. It is reputed to be superior for this purpose to fascism, communism, theocracy, imperial monarchy, and any other form of authoritarian governance that has been tried.

One of the tenets that follows from the economic premise is that governments should leave to market forces to discover comparative advantages and accordingly develop agricultural, mining, industrial, and commercial activity across regions. A complementary tenet is that global welfare will be maximized and populations that specialize in their comparative advantages discovered by markets can enjoy each others' fruits by trade with one another. Industrial Policy

A corollary conclusion is that political authorities (i.e., governments) should keep "hands off" of such specialization and trade processes. This means that they should not practice "industrial policy" to pick winners and suppress losers that do not correspond to comparative advantages. Interregional trade theory posits that failure to allow comparative advantage specialization will diminish the flow of trade and the economic welfares of prospective trading partners.

But industrial policy to attract the construction of plants has become standard procedure implemented by state and local governments in the United States in attempts to attract industry to their regions, irrespective of political affiliations of governors, mayors, and county administrators.

The comparative advantage principle is best understood with respect to what might be called the "natural" characteristics of a region, e.g., soil, terrain, location, labor, etc. It is not so clear that the principle applies to the fluidity of technological and industrial abilities that can be established by research and investment.

Two justifications for government intervention in regard to technological and industrial capabilities are to establish an advantage where none of the type previously existed, and to defend or preserve such an advantage in the face of foreign efforts to establish or pirate a similar advantage. Both the aggressive intent to establish a technological or industrial advantage and the defensive effort to prevent loss of such an advantage become matters of industrial policy.

Several exceptions to the admonition to specialize by comparative advantage are acknowledged in international trade textbooks, including the possibility that international political circumstances may override economic preferences. This has been the case in the twenty-first century as trading nations have imposed trade restraints and pursued their own policies to subsidize the local development of industries.

An international example of industrial policy accompanied by industrial espionage is that the Chinese government has sponsored the pirating of American technologies in order to enable the development of indigenous industries employing those technologies. China also threatens the technologies implemented in Tiawan to produce and export advanced silicon chips. This has led the Biden administration to promote and subsidize the expansion of the domestic silicon chip industry.

Subsidized investment to promote development of an industry in one country may have the effect of altering what otherwise may have been natural comparative advantages between that country and its trading partners. A potential loss of comparative advantage to a trading partner that has implemented technological espionage and investment to capture the comparative advantage may be sufficient non-economic reason to implement a countering industrial policy. Such industrial policy in one country may be seen to justify an opposing industrial policy in another country in the effort to preserve its comparative advantage or neutralize an emerging foreign comparative advantage.

Comparative advantage to the contrary not-withstanding, a failure to implement industrial policy at critical junctures may result in loss of comparative advantage that leaves the nation with diminished employment, income generation, and production of goods deemed essential to national security. Import

Substitution Industrialization

In the post-World War II era, governments in a number of countries, many in

Latin America and East Asia, pursued a special case of industrial policy,

import-substitution industrialization (ISI). Their intents were to contravene

their natural comparative advantages or develop new or

latent comparative advantages. The usual vehicles of ISI policy implementation

were subsidies for domestic producers and tariffs on imported goods that

would compete with domestically produced goods, with the intent of reserving

the domestic market for exploitation by domestic companies. ISI development

policies of course reduced these countries' flows of trade, with deleterious

effects on the welfares of their citizens.

The motivations to

implement ISI policies have included the desire to achieve autarky, i.e.,

internal self-sufficiency in the production of all goods and services consumed

in the region, or to give selected domestic industries a chance to develop and

“grow up” to become internationally competitive. At various times Japan, China,

Russia, and some Latin American nations have adopted ISI development policies.

In response to the sanctions imposed recently by Western nations on Russia in regard

to its invasion of Ukrane, Russia has move toward attempting to achieve

autarky.

ISI development

policies failed almost universally, not only because they contravened the

comparative advantages possessed by those nations that implemented them, but

also because they induced more imports of raw materials, machinery, and

technology than the reduction of imports that were tariffed. In almost all

cases where ISI policies have been implemented, the rates of economic grown

diminished along with their volumes of trade.

While ISI policies

attempted artificially to broaden domestic entrepreneurial opportunities

at the expense of foreign firms, they also narrowed the range of consumer

choice to higher-cost domestic goods. In most countries where ISI policies

were attempted and failed, they have been succeeded by export-oriented investment

(EOI) policies that exploit the countries' natural comparative advantages. EOI

development policies also increased the volume of trade and stimulated

economic growth in the regions where they were implemented.

While regions of the world may have macro level comparative advantages, the operatives who have to discover and exploit those comparative advantages are micro level people who function as decision making agents of business firms. It should also be noted that business decision makers can attempt to change a region's comparative advantages through implementing technological change and capital investment. The acts of discovering, exploiting, and changing comparative advantages are essentially entrepreneurial in nature.

Developing Economy Terminology

The theory of comparative advantage, now nearly universally accepted

by economists, holds that nations ought to specialize their production

in the goods and services that they can produce at lowest opportunity costs

(i.e., their comparative advantages) in order to achieve global resource

allocation efficiency and welfare maximization.

External Balance refers to a

nation's trade, investment, and official reserves transactions with the rest of

the world. A nation with an absolutely closed economy, i.e., one that is perfectly

isolated from the rest of the world, would have no external transactions to

balance. The external balance for an open economy that enjoys substantial

private sector trade and investment discretion is indicated by its Balance of

Payments.

Balance of Payments (BoP) accounting, strictly speaking, is not part of the process of accounting for

National Income and Product, but BoP accounting information feeds into the NIPA process of compiling GDP. Table 8-1 has been

designed to illustrate the structure of the BoP accounts. Information for Table 8-1 was downloaded from the Bureau of Economic

Analysis website (http://www.bea.gov/international/), but the information has

been reorganized and reformatted to exhibit a structure that is more easily interpreted. A table with more recent BoP data is

presented in the Addendum to this chapter.

For purpose of conceptual analysis, a nation's BoP

presentation requires only three sections, a Current Account section, a Capital

Account section, and an Official Reserves section. Table 8-1 exhibits a fourth

section, Discrepancy, for reasons that will be indicated below.

The Composition of Imports and Exports

Payments Imbalances

Early in the twenty-first century, the line

is most commonly drawn below the Balance on Current Account (line D in Table

8-1). Abstracting from the Discrepancy line (i.e., assuming that the

Discrepancy line total is zero), the Current Account is in surplus or in

deficit depending upon whether the sum of the nation's imports, gifts by

citizens to foreigners, and incomes earned by foreigners in the nation (all of

which involve fund outflows) is greater or lesser than the sum of the nation's

exports, gifts by foreigners to citizens, and incomes earned by citizens

overseas (all of which involve fund inflows). True balance of a nation's

Current Account occurs only when these two sums are equal and the Discrepancy

line amount is zero.

Payments Imbalance Adjustment Mechanisms

Sustainability of Current Account Imbalances

BACK TO CONTENTS

The chart below presents BoP data for Quarter 3 of 2023. The Bureau of Economic Analysis simplified its BoP presentation between 2009 and 2023 to display less detail. The letters and numbers appearing on account liness in this table correspond roughly to the letters and numbers on account lines in Table 8-1.

B. Imports of goods and services and income payments

H. Capital-account balance

Net financial transactions

J. Statistical discrepancy

The increase in exports was led by industrial supplies and materials, primarily petroleum and products. The increase in imports was led by automotive vehicles, parts, and engines, primarily passenger cars and other parts and accessories. Partly offsetting this increase was a decrease in imports of nonmonetary gold.

An exchange rate is the price of one currency expressed in terms of another

currency. During part of the twentieth century, the exchange rates of many

countries' currencies were relatively stable during some periods, but more

volatile during other periods. What causes exchange rates to change, and how do

changing exchange rates affect macroeconomies?

In Figure 9-1, the demand for the domestic currency on the forex market varies

inversely with price, €/$, as its principal determinant. The demand for the

domestic currency derives from two sources, citizens of the nation and

foreigners. Citizens of the nation may demand their own currency on the

forex market if they have acquired foreign currencies in

trade, as earnings on investments, or as gifts. The foreign demand for the

domestic currency is equivalent to the foreign supply of the foreign currency.

Foreigners may supply their own currencies to purchase the nation's domestic

currency on the forex market in order to make gifts to citizens of the nation,

import goods and services from the nation, or invest in the nation.

Assuming that the supply of dollars does not change, the increased demand

for dollars on the forex market induces the price of

the dollar to rise. This means that the dollar appreciates relative to the

value of the euro, or the euro depreciates relative to the value of the dollar.

A change in any of the non-price determinants of demand in the opposite

directions to those specified above would decrease the forex

demand for dollars. Again, assuming that the supply of dollars does not change,

the demand decrease would induce the euro price of the dollar to fall. This

means that the dollar depreciates relative to the euro, or the euro appreciates

relative to the dollar.

These demand-supply principles allow the following generalizations about the

likely direction of change of an exchange rate. Each statement should be read

through twice, once with the word to the left of the slash in each pair, and a

second time with the word to the right of the slash in each pair. Careful

attention should be paid to the ceteris paribus conditions. If "other things" do not remain the same, the

conclusion of the generalization may not obtain.

As the world economy becomes progressively more open and economically

integrated,

the vehicles for macroeconomic adjustment to internationally-sourced

disturbances attain ever greater significance. Basically, there are

only three

macroeconomic adjustment vehicles: exchange rates, domestic prices

(including

interest rates), and domestic employment (and incomes). A progression

of

"if statements" identifies the relevant adjustment possibilities:

The Demand for Money and the Demand for Exchange

The possible causes of an emerging or growing Current Account

deficit of a

nation are the same items listed above that cause depreciation of its

domestic

currency. Three of the most prominent causes are domestic incomes

increasing at

a faster pace than foreign incomes, domestic inflation at a faster pace

than

foreign inflation rates, and domestic interest rates which are lower

than

foreign interest rates.

As

noted above, the central bank may passively allow the net effects on

the

domestic money supply to have the natural price and interest rate

effects, or

it may attempt to neutralize the impact on the domestic money supply

with

off-setting monetary actions in the open markets for financial

instruments in

the nation.

In this section we illustrate with graphic models some scenarios which,

starting

from an initial equilibrium, eventually result in balance of payments

deficits.

The appendix to this chapter explores scenarios culminating in balance

of

payments surpluses.

Monetarists suggest that the bond market is not the only place where

people

can rid themselves of excess money balances. They may do so by

increasing their

consumption spending relative to the flow of their incomes so as to

decrease

their saving. Panel (c) illustrates that when people increase their

consumption

spending the aggregate demand curve shifts right (increases) from AD to

AD’.

Other things remaining the same for aggregate supply, AS, the increased

spending will induce output (and income) to rise above Y1,

and the

price level to rise above P1 as illustrated in panel (c).

The

previous section described the implications of a Current Account deficit (or a

Capital Account surplus). This section describes the implications of a Current

Account surplus (i.e., a Capital Account deficit).

Can exchange rate flexibility insulate the domestic economy from

international

disturbances? Suppose that there has occurred an

externally-sourced (foreign) decrease of demand for domestically

produced

"things" (anything, including merchandise, services, financial

instruments, direct investments, etc.). If this decreased demand

impacts

primarily the current account (merchandise and services), the result is

a

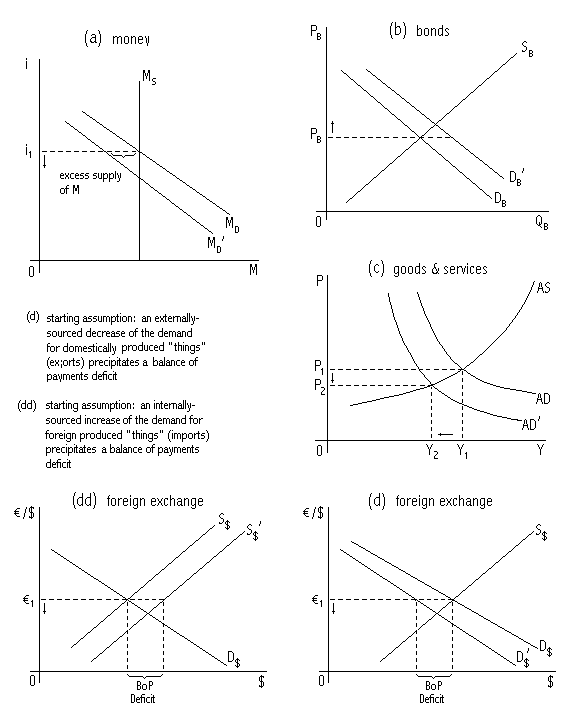

decrease of exports (X). Panel (d) of Figure 10-2 illustrates the

resulting

decrease of the demand for dollars on the foreign exchange market to

purchase

such things, precipitating an incipient balance of payments (BoP) deficit and portending a depreciation of

the exchange

rate.

In either case illustrated in panels (d) or (dd),

net exports (X - M) decreases, causing a decrease of aggregate demand

illustrated as a leftward shift of the AD curve in panel (c). To the

extent

that AD decreases, real output (Y) falls and unemployment rises.

A nationalistic sort of policy emerged in the second half of the

nineteenth

century as many of the industrializing nations of Europe and North

America resolved

to eliminate volatility in the exchange rates among their currencies by

establishing metallic standards. While the United States flirted with

gold and

silver bimetallism, it along with most other nation states settled upon

gold as

standard by the end of the century. Subscription by a nation to the

Gold

Standard was accomplished by having some government exchange-control

authority,

usually the treasury or a state sponsored bank or central bank, to

maintain the

value of the currency in terms of gold at an established (by fiat)

ratio

between a unit of the currency and an ounce of gold.

After

World War II, representatives of the governments of the victorious

Allied

nations met in Bretton Woods, New

Hampshire, to

hammer out a new exchange rate regime. While it had become obvious that

the

Gold Standard was unworkable in a world of discretionary policy, there

was

lingering sentiment favoring a metallic monetary standard as a means of

minimizing exchange risk. The system devised at Bretton

Woods constituted the U.S. dollar as the central reserve currency and

gave U.S.

monetary authorities the responsibility to keep the value of the dollar

fixed

to gold at $35 per ounce. Other nations subscribing to the Bretton

Woods system would then stabilize their currency values to the dollar.

In this

way, the risks associated with varying exchange rates would be

eliminated, or

at least minimized.

From

the end of the Bretton Woods era in 1971

until the present,

the global exchange rate system has nominally been one of flexible or

floating

exchange rates. However, governments, singly or in small ad hoc

groupings

(e.g., the Group of 7), have entered foreign exchange markets in

efforts to

manipulate one or another exchange rate. Sometimes the objective has

been to

arrest the decline or rise of an exchange rate. Occasionally it has

been to try

to push an exchange rate in a desired direction.

Managers of firms engaged in international commerce should monitor exchange

rate changes and likely governmental responses in regard to them. In countries that are suffering Current

Account deficits when exchange rates are permitted to flex, the ensuing

depreciation of the domestic currency will make domestically produced goods

less expensive to foreigners, and foreign goods will become more expensive to

citizens of the country. If

export-oriented domestic producers let the currency depreciation feed through

to their export goods prices, they can enjoy expanding sales. If they maintain their export goods prices in

order to widen their profit margins, their export sales may remain stagnant or

even decrease. The higher prices of

imported goods will cause domestic importers to suffer declining sales unless

they can offset the higher prices of foreign-made imports by cutting delivery

costs or accepting narrower profit margins.

During the 1980s and '90s it was fashionable in the media and in economics

texts as well to describe the U.S. trade deficit and the U.S. federal

government's budget deficit as the "Twin Deficits," and to

hypothesize the latter to be the cause of the former. At the turn of the

millennium, the U.S. government's budget deficits shrank to the point that

budget surpluses appeared possible, with forecasts of cumulative surpluses over

the next couple of decades sufficient to retire the entire federal public debt

of more than $4 trillion. However, early twenty-first century decreases in tax

revenues and increases of government spending caused the prospect of budget

surpluses to evaporate and deficits to become chronic and growing. By 2011, the

U.S. government's annual deficit had exceeded $4 trillion, and the cumulative

public debt was almost $15 trillion, nearly as large as the U.S. GDP. Since the trade and the budget deficits were reputed to be twins, one might

suppose that as the government's budget turned toward surplus around the turn

of the century the trade deficit might also have declined or become a surplus,

but this supposition would be wrong. Each month in the new millennium

seemed to bring a new trade deficit records (the U.S. trade deficit widened to

a record $69.86 billion in August, 2006) and the government's budget relapsed

into deficit as well, thus seeming to reconfirm the twin relationship between

the budget deficit and the trade deficit. With vague allusions about

causation, the media hardly knew how to handle the reporting of these

matters. And apparently economists were not

giving the media reporters much help in explaining the persistent and growing

trade deficit. There's still something missing from the deficits equation that

needs to be brought into the discussion. Perhaps the most straight-forward approach to explaining these matters lies

with macro theory income and expenditure concepts. From these concepts

we can deduce that the output of a nation (Y) is the sum of its personal

consumption expenditures (C), its gross private domestic investment

expenditures (I), its government purchases (G), and its exports (X) less its

imports (M), i.e., (1) C + I + G + X -

M = Y, In following discussion, we will use the convention of representing the

trade balance as (X - M) if it is a surplus, or as - (M - X) if it is a

deficit. Also from national income accounting principles we can specify that the

income (Y) generated in producing the national output can be used for

consumption spending (C), saving (S), and paying taxes (T), or (2) Y =

C + S + T. Since Y is common to both equations, we may set the left side of equation

(1) equal to the right side of equation (2), (3) C + I + G + X - M = C + S + T. The two Cs cancel each other. With substitution of

- (M - X) for the trade balance and rearranging terms, the relationship

becomes (4) (I - S)

+ (G - T) - (M - X) = 0, or (4') (I - S)

+ (G - T) = (M - X). Assuming that the value of the first variable exceeds the value of the

second variable in each set of parentheses, the three terms in parentheses can

be interpreted as a domestic saving deficit (I - S), a budget deficit (G - T),

and a trade deficit (M - X). The saving deficit, (I - S), alternately can be regarded as an

"investment surplus." The larger the

investment surplus the better because investment is the vehicle for

implementing new technologies, adding to the capital stock, and generally

enhancing the productivity of the labor force. But (I - S) also

has a negative implication when domestic saving is inadequate to finance all of

the investment that is being undertaken. Additional investment financing

sources are needed. The sense of equation (4') is that a combination of a saving deficit and a

budget deficit must equal (or be financed by) a trade deficit.

Alternately, a trade deficit enables either or both of a saving deficit and a

budget deficit. As long as the saving deficit is trivial in magnitude,

then it follows that the trade deficit must be approximately equal to the

budget deficit. While it is not clear that either is dominant and the

other accommodative, a seemingly safe presumption is that the U.S. government's

post-World War II budget deficits resulted from the political process, and that

the trade deficits emerged to finance the budget deficits. In any case,

during the 1980s the two deficits appeared to be twins, with a change in budget

deficit eliciting a same-direction (though not necessarily simultaneous) change

in the trade deficit. During the late 1990s, the U.S. government's budgetary deficits shrank with

on-going economic growth (often described in the media as a "torrid

pace" that exceeded 7 percent per annum during some quarters toward the

end of the decade). By 1999, the U.S. government's budget approached the

realm of surplus. A budget surplus may be represented as - (T - G), so

that equation (4') may be rearranged as (5) (I - S) - (T - G) = (M - X) or (5') (I - S)

= (M - X) + (T - G). This equation suggests that a saving deficit could be financed by the sum of

the trade deficit and the emerging budget surplus. During the late-1990s

the trade balance and the budget balance appeared no longer to behave as twins.

As the twentieth century wore on to its conclusion, the saving deficits

ceased to be trivial. During the last couple of decades of the twentieth

century, U.S. gross private domestic investment has grown faster than has

domestic saving as officially measured. The official measure of saving is

disposable personal income (DPI) less consumption spending (C). This measure

ignores saving in the form of wealth accumulation and saving after the fact of

consumption spending in the form of debt amortization payments. Early in

the twenty-first century, the measured U.S. saving rate approached an historic

low (negative during some quarters) even as investment boomed. The growing

saving deficits have been accompanied by federal government budget deficits of

varying magnitudes. The two together require a commensurate trade deficit

to finance them. Around the turn of the third millennium the deficits became

triplets. The dominating factor of the late 1990s in the U.S. appeared to be a communications

and computing revolution of force similar to that of the Industrial Revolution

in late nineteenth-century England. The salient economic feature of this

"New Industrial Revolution" was an ever-growing U.S. saving deficit

that has had to be financed by a combination of a growing trade deficit and/or

an increasing government budget surplus. The late '90s declining budget

deficits were produced by an increase in tax revenues as both the personal and

corporate income tax bases increased with the "torrid pace" of U.S.

economic growth. Supply-side restructuring of the U.S. economy during the

1980s also may have been an enabling condition to the unfolding of the

"New Industrial Revolution" of the 1990s. Declining budget deficits during the late 1990s decreased the government's

demand for loanable funds in the U.S. The

potential for budget surpluses at the turn of the century began to decrease the

demand for loanable funds as the government required

smaller amounts from the capital markets. The decreasing deficits of the

late 1990s might have been expected to decrease U.S. interest rates.

However, soon after the turn of the new century the U.S. central bank (the

Federal Reserve) resolved to increase nominal interest rates in an effort to

slow the pace of growth of the U.S. economy to a "sustainable level"

and avert inflationary pressures. A by-product of the Federal Reserve's actions to increase nominal U.S.

interest rates is that they have become higher than comparable rates in Europe

and the Pacific Basin, and this relationship has induced a flow of funds into

the U.S. in search of higher returns. The inflow of funds has increased

the demand for dollars and the supplies of other currencies on the foreign

exchange markets, thereby causing the dollar to appreciate relative to other

currencies. In addition, the administration continued to indulge in

rhetoric favoring a "strong dollar policy." By 2005 there was growing

concern in some quarters that the dollar had become overvalued. The dollar

appreciation made American goods appear more expensive to foreigners, with a

consequence of declining U.S. exports. At the same time, the stronger

dollar made foreign goods look cheaper to Americans, thereby causing U.S.

imports to increase. The combination of the tighter monetary policy and

the dollar appreciation has resulted in growing trade deficits that have served

to finance both the growing saving and government budget deficits. And then the U.S. economy suffered the so-called Great Recession that began in

2008. Macropolicy stimulus programs swelled the government?s budget deficits and accordingly increased

the public debt to historic levels. As the recession ensued, business

investment collapsed, reducing the saving deficit. The U.S. economy?s

trade deficits began to ameliorate as the U.S. income level fell, but continued

to help finance the government?s growing budget

deficits. It may be obvious how a government budget surplus could help to finance a

saving deficit, particularly when the surplus is used to retire public debt,

but how can a trade deficit help to finance a saving deficit? In order to

explain this, it would be a convenience to interpret the trade balance as the

Current Account in the nation's Balance of Payments. The nation's Balance

of Payments is comprised of three sections, the Current Account, the Capital

Account, and the Official Settlements Account. The Current Account is

comprised of three subsections: the Trade Balance, Net Unilateral

Transfers (i.e., the net of gifts by citizens of the nation to foreigners less

foreign gifts to citizens of the nation), and Net Income Earned Abroad (i.e.,

the net of income earned abroad by citizens of the nation less income earned in

the nation by foreigners). Since net transfers and net income earned

abroad are of relatively minor magnitudes and tend to offset each other in the

U.S. economy, the trade balance, (X - M) or - (M - X), accounts for the bulk of

the U.S. Current Account. We shall thus ignore net transfers and net income

earned abroad so as to treat the Current Account balance solely as the trade

balance. In a fixed exchange rate system such as the pre-Depression Gold Standard or

the post World War II Bretton Woods System, flows of

gold or international reserves were necessary to keep the exchange rates of the

subscriber nations' currencies unchanged vis-à-vis gold or other

currencies. A byproduct of the process of fixing exchange rates was that

the Current Account and the Capital Account balances for a nation could differ

in amount totals, with the difference being made up in the Official Settlements

Account. Since the early 1970s, the world has been on a nominal flexible

exchange rate system, though one in which governments of nations occasionally

attempt to manipulate exchange rates. If exchange rates were completely free to vary in response to market forces,

the Official Settlements Account total for each nation would be zero because

exchange rates would change to bring about an equivalence of the Current Account

total with the Capital Account total, or vice versa. A Current Account

deficit must be offset by a Capital Account surplus, and vice versa. If a

nation imports more from the rest of the world than it exports to the rest of

the world, the nation must export the ownership of enough capital to "pay

for" the trade deficit. In fact, the U.S. has experienced trade

deficits through most of the years beyond the early seventies when flexible

exchange rates became a reality. The Current Account deficits necessarily

have been offset by Capital Account surpluses. A Capital Account surplus may be comprised of a combination of long term

capital exports (e.g., foreign purchases of stocks, bonds, and real assets in

the U.S.) and exports of short term instruments (e.g., increased foreign

ownership of U.S. bank account balances and other liquid financial

obligations). The Capital Account balance must be the negative of the

Current Account balance when exchange rates are flexible. It is in this

sense that a Current Account deficit (most of which is composed of the trade

deficit) can help to finance a saving deficit. The corresponding Capital

Account surplus involves a net export of the ownership of capital, which is the

same as to say an inflow of funds from abroad. A trade deficit (a Capital

Account surplus) is thus a natural concomitant of a saving deficit, and is

necessary to help (along with a government budget surplus) with the financing

of the saving deficit. A saving deficit can be financed by a combination of budget surplus and

trade deficit. But if the budget is also in deficit, there is an even

greater burden on the trade deficit to finance both the saving deficit and the

budget deficit. How is this "financing" of the saving and budget

deficits brought about by a trade deficit? Market economies contain within

themselves adjustment forces that are invoked when prices or incomes are too

high or too low for equilibrium. These forces of adjustment are the unmet

intentions of market participants. Prices are the primary adjusters of

the market economy, but if prices change too slowly or are fixed or manipulated

by government authority, income (and correspondingly output and employment)

will become the shock absorbers of the market economy. Two prices that play crucial roles in the macroadjustment

of the market economy are interest rates and exchange rates. Interest

rates vary in response to changes in the demand for and supply of loanable funds, and the interest

rate changes elicit equilibrating changes in saving, investment, output, and

employment. However, if interest rates are fixed or manipulated by

government authority, excess demand or supply in the loanable

funds market will persist. The natural and inherent forces within the

economy will be prevented from bringing the trade balance (X- M) into

equivalence with the saving (I - S) and government

budget (G - T) balances. Much the same can be said for exchange rates because they are no less than

the prices of the nation's currency expressed as quantities of other currencies

for which it can be exchanged. Exchange rates vary in response to changes

in the demand and supply of the nation's currency on foreign exchange

markets. Currency demand and supply changes are invoked by changes in

income levels, price levels, and interest rates among nations. Exchange

rate changes are the crucial vehicles of adjustment of the trade balance to the

saving balance and the government's budget balance. Changes in either the

saving balance or the budget balance will initiate changing demand or supply

for the nation's currency, and thereby elicit exchange rate changes that ensure

equilibrating (and offsetting) changes in the Current Account and the Capital

Account of the nation's balance of payments. If exchange rates are fixed

or adversely manipulated by government authority, excess demand or supply of

the nation's currency will persist, and the Current and Capital Accounts will

not be brought into balance with each other or with the saving and budget

balances. We can offer several comments on the prospects for stability of the U.S.

economy during the early years of the twenty-first century. 1. At the turn of the third millennium, the U.S. government budget

surpluses did not become large enough to provide significant financing of the

growing U.S. saving deficit. The burden of financing the increasing

saving deficit thus still falls principally upon the trade deficit and is

aggravated by the persistent government budget deficits.[1] Early twenty-first

century tax cuts and expenditure increases appear to have eliminated the

possibility of budget surpluses and the retirement of public debt. Even

though the tax cuts may have given the population some more disposable income,

it appears that the saving rate has not increased relative to the investment

rate so as to diminish the saving deficit. Indeed, the national saving rate has

continued to fall as the economy has weathered the so-called "Great Recession"

that ensued in late 2008. The political issue has become whether to let the

2002 tax cuts lapse, which would amount to a tax increase as the economy

continues to suffer recessionary conditions. 2. The "New Industrial Revolution" boom came to an end by

the turn of the third millennium, but the U.S. growth rate was sustained

moderately well until the start of the "Great Recession" in

2008. After an actual decline in GDP during 2009, weak growth resumed in

spite of massive monetary policy injections of liquidity into the U.S. economy.

Persistent unemployment and stagnant or falling incomes have resulted in

declining trade deficits as imports have decreased. 3. A rising tide of protectionism in the U. S. has elicited demands

for new or higher tariffs, new or more stringent import quotas, and other

non-tariff barriers that might force a decline of the trade deficit. The

regrettable side effect of this protectionism would be to force a diminishment

of the saving deficit (due to a decrease of investment spending) that propelled

the "New Industrial Revolution" boom unless the government's budget

can be brought into surplus (which seems highly unlikely). 4. The U.S. government acting solo or in concert with a group of other

nations (e.g., the G8 or some other number of cooperating nations) may resolve

to prevent further appreciation or precipitate depreciation of the U.S. dollar

relative to other currencies. The dollar has experienced moderate

depreciation during the "Great Recession,” and

the dollar depreciation has stimulated U.S. exports and constrained U.S.

imports to cause the trade deficits to decrease. The U.S. government has urged

appreciation of other currencies (particularly, the Chinese yuan)

in the interest of promoting U.S. exports and constraining its imports.

With rising government budget deficits, future growth of the U.S. economy

continues at risk unless the U.S. saving rate can somehow be increased to

finance continuing domestic investment. 5. If the Federal Reserve is given responsibility for forcing further

depreciation of the dollar, it can do so only by sacrificing domestic monetary

policy to the achievement of the exchange rate goal. The foreign

currencies can be purchased only with monetary expansion that inevitably will

elicit global inflation as a byproduct of the forced dollar depreciation.

With recent monetary expansion, U.S. interest rates have fallen to historic

lows, inducing an outflow of funds in search of higher yields abroad. For

better or worse, the dollar has edged ever closer to becoming a global common

currency even as the dollar depreciates. If the saving rate cannot be increased so as to diminish the saving deficit,

the trade deficit might be diminished by sustained and accelerating growth

(another "New Industrial Revolution"?) that yields governmental

budget surpluses that can help to finance the saving deficit. However, by late

2008, the U.S. economy had entered the "Great Recession" and budget

deficits increased. By 2010 the cumulative public debt eclipsed $1 trillion,

but trade deficits were diminishing. With persisting U.S. government budget deficits and governmental

manipulation of interest rates and exchange rates, the economy's automatic

adjustment mechanisms may not be able to bring about either a falling U.S.

saving deficit or a declining U.S. trade deficit. If not, the triple deficits

will persist into the foreseeable future and are likely to aggravate

imbalances. [1] If the budget surpluses had continued to mount and the U.S. public debt had diminished, the trade deficits might have declined as the burden of financing the saving deficit shifted toward the budget surplus. A budget surplus thus could have played a positive role in substituting public saving (forced by taxation) for inadequate private saving, and if the public saving were returned to the loanable funds market in the form of public debt retirement.

BACK TO CONTENTS

Our survey of global commerce begins with a half-serious apology for including a discussion of the international dimensions of business. The reason for the apology is that in much of the rest of the world outside of the United States of America, there is little significant distinction between international and domestic business operations. If one is in business at all, he or she automatically engages in international business operations. Managers of such firms hardly give second thoughts to the requisites for sourcing supplies, selling products, or locating production in countries other than that within which the firm's home office is located.

The apology is only half serious because many people in various countries, and notably the United States of America, are somewhat intimidated by the international dimension. It is a mixed blessing to the United States that it has a rich endowment of natural resources and a huge internal economy. Domestic firms have been able to rely upon the internal economy for both sources of supply and markets for their domestically-produced products. Because they have been able to look inward for over two centuries, managers of American firms have tended to regard the outside world as marginal or peripheral to their activities. Many view the international sector as possessing some mystique that requires special capabilities to penetrate. This perception is enhanced by the fact that Americans are for the most part monolingual. Although English is the only language spoken and understood by the majority of Americans, Spanish may yet overtake English as the American lingua franca.

The Increasing Importance of International Commerce

If much of American business has seemed intimidated by international involvements, post-war American consumers have carried on a love affair with foreign-made goods and services. During much of the post World War II era, U.S. balance of payments deficits have been the rule rather than the exception. Concerns about on-going trade deficits and mounting international debt to foreigners have led various U.S. governmental agencies to devise programs to promote exports and discourage imports. American experience with protecting domestic industries from foreign commercial incursions spans more than two centuries.

On-going trade and payments deficits and official concern about them have aroused the interest of the American academic community in international commercial relations. Beginning in the 1970s, a deliberate effort was mounted by business studies programs to internationalize their curricula. The most commonly used models for such internationalization efforts have been to employ foreign faculty and recruit foreign students, to introduce new courses focusing upon international business problems and procedures (e.g., international marketing, international finance, international management), and to infuse international concepts into existing courses as appropriate. The latter two models have spawned a flock of new textbook titles as well as revisions of existing texts to incorporate references to the international arena.

In a sense, the recent obsession of American commerce and academia with anything international is only a transitional phase. With the passage of time, international commercial activity will become more commonplace; eventually business studies curricula will become sufficiently internationalized that special commentary about the international sector will no longer be warranted. Three phenomena militate in favor of this transition. (1) Technological advances in communications and transportation shorten the time and costs of distance, thereby diminishing market imperfections and facilitating international exchange. (2) English, the language spoken by the majority of Americans, seems to have emerged as the global language of commerce as well. (3) Efforts underway in various regions of the world to achieve both economic and political integration (the European Union, a "single market" by 1993, currency union by 1999, and a "United States of Europe" by some point in the twenty-first century) tend to render concepts of the international ever less significant. But until such transformation is completed (if ever), we shall be compelled to include chapters such as this in our texts.

Bases for Interregional Commerce

John Donne has said that "No man is an island, entire of itself..." (Devotions upon Emergent Occasions, Meditation 17). It is surely true that no nation can be an island completely unto itself either. Some have tried. After both its Revolutionary War and World War I, the United States seemed to withdraw into isolationism in order to avoid further international entanglements, both political and commercial. After its establishment in 1918, the Union of Soviet Socialist Republics (U.S.S.R.) pursued a de facto strategy of autarky, i.e., internal self-sufficiency. Of all of the nations in the world, these two might have come closest to functional autarky because of the immense richness of their natural resource endowments. But neither of these nor any other nation in the world has been able to achieve absolute autarky. There are several fundamental reasons why they have found it either necessary or beneficial to engage in international commercial relations.

In recognition that the so-called "pure theory of trade" abstracts completely from references to nation states, we need to make a transition from the language of "international trade" to that of "interregional trade."

It is a fact of physical nature that resources are unequally distributed across the earth's geographic space. Some resources approach ubiquity (found everywhere); others are concentrated by regions. Resources that are found in only one or two places on earth may be referred to as geographic uniquities. Examples include rare elements or precious gems or metals, agricultural commodities that grow only under very special conditions, and natural tourist attractions. Populations of regions possessing such uniquities are fortunate in having access to such resources which they are able to exploit; populations elsewhere are correspondingly unfortunate. Populations of regions devoid of such uniquities may acquire them (or things produced using them) by engaging in interregional trade or military aggression to capture them.

There are few perfect ubiquities or uniquities among productive resources. Most resources are found in many places across the globe, although in greater or lesser geographic concentrations. Goods and services requiring those resources as inputs may be produced more cheaply in regions where they are found in abundance than in other regions where they are scarce.

The Principle of Comparative Advantage

Economists have enunciated the so-called principle of comparative advantage to explain regional specialization in the production of goods and services. According to this principle, people in each region should specialize in producing those goods and services that can be produced most efficiently in their region compared to other regions. "Most efficiently" means at least opportunity cost (in terms of other goods and services foregone) compared to the other regions. Since the production of goods becomes geographically specialized, people in different regions must trade their specialties for the specialties of people in other regions.

Generalization in consumption is enabled everywhere through trade even though there is regional specialization in production. It can be shown with theoretical exercises as well as empirical information that those who specialize their production according to the principle of comparative advantage and trade with one another enjoy higher welfare than they would under conditions of autarky.

It is sometimes suggested that there are regions of the world that are essentially devoid of productive advantages, whereas other regions seem to possess all of the advantages (veritable "Gardens of Eden"). We can resolve this problem by further refining the definition of comparative advantage. A region's absolute advantages include all of those things that it can produce at lower opportunity costs than can be achieved in other regions. A region's absolute disadvantage is anything that can be produced elsewhere at lower costs in terms of other goods and services which must be foregone.

It may well be that opportunity costs of most things are lower in one region relative to all others, but this does not mean that the region should generalize in production. Its comparative advantages lie in those things for which it has greatest absolute advantage(s), while the comparative advantages of other regions lie in the things for which they have least absolute disadvantages. They should still specialize in production, but the one in its greatest absolute advantage and all the rest in their least absolute disadvantages. It follows logically from this definition of comparative advantage that it is not possible for a region to have no comparative advantage(s). Furthermore, it can be shown that all of the regions of the world, the sparsely-endowed as well as the abundantly endowed, will enjoy higher welfare with specialization according to the principle of comparative advantage and trade with one another unencumbered by politically imposed constraints.

Modern elaborations of the theory of comparative advantage recognize at least five bases for regional comparative advantages: resource endowments, cultural preferences, known technologies, scale economies, and company-specific knowledge. The first three are endogenous to locale; the last two technically are independent of geography, but may become location specific at the discretion of production decision makers.

For purpose of illustration, it is usual in trade theory to hypothesize a two-resource, two-commodity, two-region world. Suppose one of the regions, A, is abundantly endowed with capital resources but has only enough labor to operate its capital stock, and that the other region, B, is abundantly endowed with labor but has a small amount of capital that serves as minimal tools for the labor. The two regions produce two commodities, X which under technologies known in both regions requires a great deal of labor but not much capital, and Y which uses substantial amounts of capital but only a little labor. If the two regions employ identical technologies for producing the two goods and further have identical preference functions, region A should specialize in producing good Y, whereas region B should produce more of good X. Each should trade some of its specialty to the other in exchange for some of the other's specialty.

Suppose that the two regions have identical resource endowments and know the same productive technologies. While people in both regions consume both goods, suppose that people in region A have a stronger preference for X, the labor intensive good, while people in region B like Y, the capital intensive good. In this case, it would be appropriate for region A to specialize in producing X and region B in producing Y. Each should trade some of its output to the other in order to achieve consumption generalization in both regions. In this case, the basis for comparative advantage is differential preferences rather than resource endowments.

As a third possibility, suppose that the two regions possess identical resource endowments and share a common preference system, but that scientists and engineers in region A have advanced technology with respect to the production of X so as to economize on labor, whereas common technology continues to be used in the production of Y, the capital intensive good, in both countries. Again, intuition suggests that region A should specialize in the production of X leaving region B to specialize in production of Y. They should trade some of their respective specialties to each other. The basis of comparative advantage here is differential technologies rather than resource endowments or preferences.

It would be highly unlikely in any of these cases that perfect specialization (i.e., only X is produced in A and only Y is produced in B) would result. Both goods would continue to be produced in both regions, but in each region more of the comparative advantaged good would be produced, and less of the comparative disadvantaged good(s). Also, the real world is composed of many regions, some of which are similar to others in respect to resource endowments, preferences, or technologies, and different from the other regions in various respects. The basis for comparative advantage of each may lie in one of these areas or a combination of them. Empirical evidence suggests that a larger volume of the world's trade is conducted among regions that are similar in income levels and preferences, than among regions that are widely divergent in any of these areas.

Qualifications to the Principle of Comparative Advantage

Managerial opportunities and threats are to be found in almost any circumstances, including those of interregional trade. We must note certain qualifications to the argument presented to this point. One is that comparative advantages, whether attributable to resource endowments, preferences, or technologies, are not "struck in stone," i.e., they are changeable. Circumstances of resource depletion can terminate a former comparative advantage based on the richness of a resource endowment. The discovery of a new deposit or pool of a natural resource can confer a comparative advantage. Population growth or immigration may confer a comparative advantage in producing labor intensive goods where one formerly did not exist. By the same token, emigration may result in depletion of a former comparative advantage based on labor abundance. Natural disasters such as a volcanic eruption, a hurricane, or a freeze that destroys a crop stock may bring to an end some historic comparative advantage. Changing preferences away from "old" goods and toward newly developed ones may shift comparative advantage from regions specializing in the "old" and toward regions specializing in the "new."

The forms of comparative advantage transition noted above follow from natural or market phenomena that are not under the control of the firm. One of the most significant forms of change in comparative advantages comes about through technological advances that develop new items or new processes that economize on scarce resources. Another significant phenomenon which may change comparative advantage is capital investment. Regions that formerly were capital scarce may become capital abundant, as for example the newly industrialized countries ("NICs") of South Asia. The reason that these two forms of comparative advantage transition are significant to managerial decision making is that they are implemented at the discretion of managers of firms. It is by mounting an effort at research and development (R&D) or by capital investment that managerial decision makers may seize entrepreneurial opportunities and deliberately change the competitiveness of their firms and the comparative advantages of their regions.

The International Dimension

To this point we have been discussing interregional trade; in the so-called "pure theory of trade" (the subject matter of Chapter 2) there is no distinction between interregional and international trade. The emergence of national identity and the nation state over the past four centuries have enabled two additional factors which provide for regional differentiation: nationalism and the operations of government.

The interests of governments in international commerce have necessitated another qualification to the comparative advantage theory. The government may attempt to protect an old domestic industry in order to preserve a comparative advantage that is fleeing to foreign regions. The government may attempt to neutralize another region's comparative advantage, or it may take "compensatory" action to offset some policy being implemented by the government of another region. In any of these cases of protection, the effect will be to diminish any potential for gain by comparative advantage specialization. Governmental roles in regard to international trade are further elaborated in Chapter 4.

National identity leads to nationalism, a sort of emotional cement that binds together people of the same cultural background. They may share a common history and heritage; they may be more-or-less homogeneous with respect to race and ethnicity; typically they subscribe to the same religion or various sects or denominations of a common religion; the vast majority of them speak the same language; and, most importantly, they share a common vision about what it means to be a citizen of the nation. The term is often used to describe a "nation of people" or simply "a people" in the biblical sense (the "Children of Israel" in the Bible are an example of a nation in this sense). The emotional cement of nationalism may reveal itself in the form of patriotism, i.e., love of homeland, its cultural and political heritage, its flag.

Other terms such as provincialism or regionalism may attain almost the same sense of nationalism, but with respect to the attitudes of people in more restricted geographic locales. Belgians typically are much more nationalistic with respect to being Flemish or Walonian than they are about being Belgian. It is more important to some in the United States to be Texans or Southerners than it is to be American. The European Union is attempting to establish a sort of super-national regionalism so that citizens of the fifteen member states will begin to feel a sense of European nationalism that eventually may displace nation-state nationalism. Although there is no good term to describe it, a similar emotional cement often exists among the students and alumni of an American state university, especially when in athletic competition with a rival state university.

Nation states are political entities defined by boundaries encompassing areas that may coincide closely with that populated by a "nation of people" in the biblical sense. Sometimes a nation state encompasses two or more nations of peoples. American Indian tribes have often been referred to as "nations;" there were many nationalities in the former Soviet Union; modern India encompasses numerous tribal peoples. In the early 1990s, the various nationalities contained by both the Soviet Union and Yugoslavia began to pull apart.

Occasionally political boundaries separating nation states divide peoples of the same nationality. The post-war political division of Europe left the German people separated by "walls" as well as borders. In South Asia, the Bengali tribal people are split by the India-Bangla Desh border. The Pakistan-Afghanistan border divides the Baluchi people, while the Pakistan-India border separates Punjabi tribal people. Separatist movements in these and other areas may have as their goal the reunification of peoples of the same nationality that have been separated by political boundaries.

Nation states also may not coincide with economic regions that are characterized by the possession of natural resources. Both the United States of America and the Russian Republic include numerous uniquely definable economic regions. Sometimes national boundaries split a common resource endowment region. Europeans have often redrawn national boundaries across the rich coal and iron deposits of the Alsace-Lorraine region.

The essential characteristic of the nation state is its possession and exercise of national sovereignty by the government of the nation state. "National sovereignty" means that the government of the state has the authority and the power to do anything it wishes with respect to the peoples and resources contained within its political boundaries. This power includes the ability to determine the form of economic organization of the economy of the state (until recently, the government of the former U.S.S.R. mandated socialism), and to impose protectionist measures with respect to the industries within the economy (the government of the U.S.A. has a long history of protectionism). It includes the right to insist upon the use of a national currency within the realm and to exclude the of currencies preferred by others. Sometimes this authority and power leads to human rights abuses to which people and authorities in other nation states raise objections. Such exercise of discretion by the state is constrained only by the tolerance of its citizens and by attitudes and military prowess of other nation states.

Currency Diversity

One of the most critical factors that sets international trade apart from interregional trade is a consequence of the exercise of national sovereignty: the use of different currencies in different nation states. Because the dollar in used in the U.S. economy while the pound sterling is accepted exclusively in the United Kingdom, the balance of payments between the U.S. and the U.K. is important to economic and political considerations in both countries. The dollar-sterling exchange rate is critical to the volume of goods and services entering into international commerce between the two countries at any point in time.

Where the same currency is used throughout a region, these matters become irrelevant. In the United States, who is concerned about the balance of payments between South Carolina and New York? And what about the exchange rate between the currency used in South Carolina and that accepted in New York (both use the U.S. dollar)? In the European Union the British still insist upon using the pound sterling while the rest of the E.U. member states use the euro. The U.K.-French and U.K.-German balances of payments continue to be issues, as does the sterling-euro exchange rate. This is true especially since governments in some of the E.U. member states might prefer to stabilize the sterling-euro exchange rate while the U.K. government is inclined to allow exchange rate fluctuation as the means of correcting balance of payments disequilibria between the U.K. and the E.U.

Currency matters spill over upon the commercial sectors of the international trading partners. Balance-of-payments issues become irrelevant in Europe among the member states that use the euro. But there still will be balance-of-payments problems between the U.S. and Europe and with the dollar-euro exchange rate until such time that Americans and Europeans can agree to use a common currency.

The Cultural Dimension

The analysis of nationalism would be much simpler if every nation state were associated exclusively with a certain nation of people. But as we have already noted, this is not the case. Whether we are speaking of the nation state or a particular nation of people who share a common heritage, the principal implication of nationalism is that there are significant differences among populations that yield important consequences for trade and the location of economic activity. These differences may spring from natural phenomena such as heritage, customs, language, etc., or they may be artificially imposed by the behavior of the governments of the nation states.

Even if political relationships are not involved, differences of national heritages and languages lead to suspicions about the customs and intentions of "foreigners," and in extreme cases to xenophobia, i.e., fear and hatred of foreigners. An extreme economic consequence of xenophobia is the attempt to achieve autarky. The important point is that nationalism, whether emanating from cultural differences or state sovereignty, tends to diminish the potential for gains from interregional and international specialization and trade. In the extreme, nationalism can completely eliminate such potential gains if sovereign national governments pursue strategies of extreme political isolation and economic autarky.

Because of nationalism, it is necessary to recognize that comparative advantage may be based upon preferences that differ by regions which are defined by national boundaries as well as by cultual heritage. It is also necessary to note that natural comparative advantages may be enhanced or neutralized by the discretionary actions of government officials.

>

The managerial implications of nationalism, whether based in cultural differences or the exercise of state sovereignty, is that business decision makers wishing to buy, sell, or produce in other countries must come to an understanding of the cultural characteristics and governmental practices of the other countries. It is these differences that make foreign dealings appear to be mysterious, difficult, and risky. The antidotes are acquaintance and familiarity with the foreign environments within which the firm expects to operate. Acquaintance and familiarity can be achieved through study, travel, and interaction with nationals from the target markets. The study should include examination of cross-cultural differences that lead to appreciation of customs and practices different from one's own.

One of the best ways to achieve such appreciation is to learn the languages of the peoples who live in the regions where the firm wishes to operate. Competence in the languages of the target markets may also be crucial to successful business dealings. Peoples in most countries of the world are multilingual; in some few countries (notably the United States) the norm seems to be monolinguality. A business negotiator who is knowledgeable of the trading partner's language as well as his or her own will likely have the upper hand over a negotiator who speaks only one language. Also, if one is not familiar with the trading partner's language, the partner will be able to lapse into his or her own language when speaking with associates. Finally, we may note that most people in other lands have greater appreciation of their trading partners if they can at least attempt to speak the local language.

BACK TO CONTENTS

Factor Intensity

The analysis begins with production isoquants for a product produced in a region. An isoquant is a path in graphic coordinate space along which various combinations of capital (K) and labor (L) yield the same level of output. An isoquant map showing two representative isoquants (among an infinite number of such isoquants that could be shown), all other inputs accommodating the K and L input requirements, is illustrated in Figure 2-1.

Figure 2-1.